Largest Price Drop This Year

Largest Price Drop This Year

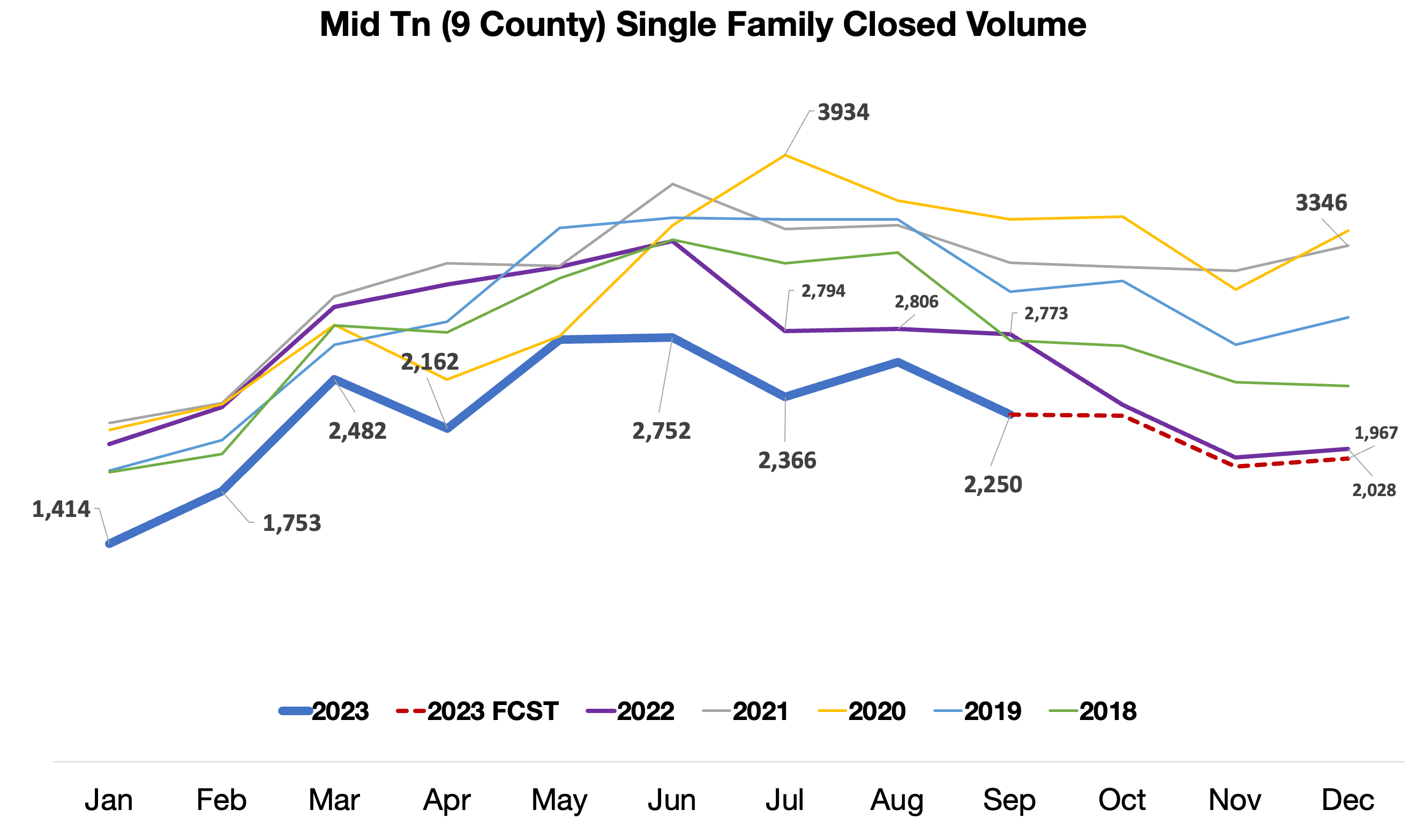

September Results and Key Data Points

A lot happened in September but the most notable was the dramatic move in prices.

Happy Thursday, GNR should be releasing their data points soon and this is what I expect them to post for Single Family Homes:

(small variances possible depending on exact timing of pull)

Median Sales Price: $467K Down a whopping 2% MoM and down 6.6% from last year’s peak of $500K (May 2022), and down 1.7% YoY.

Inventory: 6,789 (Active Listings + Under Contract - Showing) vs last year 7,005 - inventory as reported could show a slight decrease. One interesting note is that prices are falling rapidly even as lower priced inventory remains much tighter than last year. So if you hear the narrative prices can’t fall because of supply, just know, we have enough supply for prices to fall.

Close Volume: ~2,250 down 19% from last year’s 2,773, Month over Month down 13% from 2,591 in August. The YoY drop is significant, because last year September was already much lower than normal, so another 19% is feels unprecedented.

Contract volume is also low suggesting that October closed volume could be flat to down YoY.

Paid Links below: Assumable Listings, New Build Map, Aged Inventory Map, Price Band Inventory Maps